1 month ago

11

1 month ago

11

On March 24, 2025, Galaxy Digital agreed to pay a $200 million settlement to the New York Attorney General’s Office to conclude an investigation into its involvement with the Luna cryptocurrency. This sum serves as a penalty, effectively a price to halt the NYAG’s probe.

Initially, I intended to discuss how Galaxy allegedly used Luna to defraud its supporters by inflating its value and then selling off holdings. The NYAG’s documents provide detailed insights into Galaxy’s simultaneous promotion and liquidation of Luna.

One notable detail is how Mike Novogratz, Galaxy’s CEO, used a tattoo to promote Luna.

March 26, 2021: Novogratz tweeted that he would get a Luna tattoo if its price surpassed $100.

March 26, 2021: Novogratz tweeted that he would get a Luna tattoo if its price surpassed $100. December 24, 2021: He announced on Twitter that Luna had reached $100 and he was seeking inspiration for a “cool tattoo” to commemorate the milestone.

December 24, 2021: He announced on Twitter that Luna had reached $100 and he was seeking inspiration for a “cool tattoo” to commemorate the milestone. January 4, 2022: On the same day he sold 165,000 Luna tokens at an average price of $86, Novogratz posted a photo of his new Luna tattoo, which sparked widespread enthusiasm.

January 4, 2022: On the same day he sold 165,000 Luna tokens at an average price of $86, Novogratz posted a photo of his new Luna tattoo, which sparked widespread enthusiasm.

However, he did not mention his sale of Luna in these posts.

This raises questions about such contradictory behavior and the lengths individuals might go for financial gain. More concerning practices will be discussed in due course.

The pressing question is:

Is Galaxy being treated unfairly? Did Novogratz deceive investors?

While this may seem odd, numerous Key Opinion Leaders (KOLs) have voiced support for Novogratz.

1. KOLs Defend Galaxy

Galaxy Digital’s $200 million settlement has sent shockwaves through the crypto community, eliciting strong reactions from prominent KOLs. Many have expressed sympathy and support for Novogratz on platforms like Twitter and podcasts, with some labeling the case as a form of “judicial extortion.”

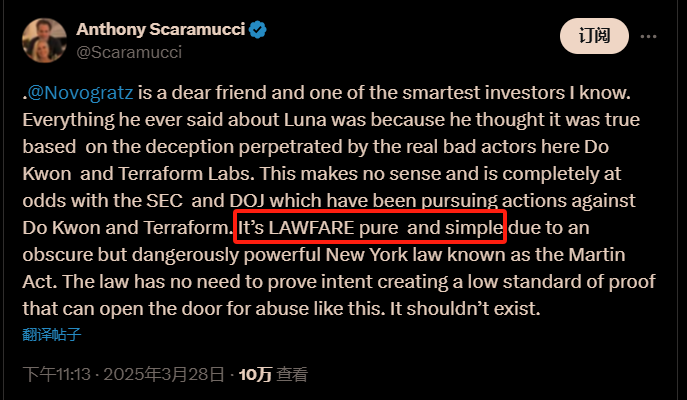

The most notable defense comes from Anthony Scaramucci, founder of SkyBridge Capital, known for his sharp rhetoric. His comments have attracted media attention, with Cointelegraph headlining: “NAYG lawsuit against Galaxy was ‘lawfare, pure and simple’ — Scaramucci.”

On March 28, Scaramucci tweeted that the lawsuit was purely “lawfare,” a blatant act of judicial bullying. He criticized New York State’s use of the overly broad Martin Act, which allows the Attorney General to act without proving fraudulent intent, compelling companies to settle. This tweet quickly garnered thousands of retweets and likes, sparking widespread discussion in the crypto community.

The controversy centers on the Martin Act, which grants the Attorney General special privileges to act without proving fraudulent intent, leading to Galaxy’s $200 million “ransom.”

So, what exactly is the Martin Act that Scaramucci refers to?

2. The Martin Act

To understand why Galaxy Digital agreed to a $200 million settlement, it’s essential to grasp the origins and implications of the Martin Act, described by Scaramucci as a tool of “judicial bullying.”

Enacted in 1921, the Martin Act, formally known as New York General Business Law Article 23-A, is considered one of Wall Street’s most stringent weapons and is now causing a stir in the crypto world.

2.1 Why Is the Martin Act Considered So Severe?

The Martin Act grants the New York Attorney General (NYAG) extensive investigative and prosecutorial powers over securities and commodities fraud within the state. Its severity stems from two key aspects:

No Need to Prove Fraudulent Intent (Scienter): Unlike typical securities fraud cases that require evidence of intent to deceive, the Martin Act allows the NYAG to proceed if a defendant’s actions have the potential to mislead investors, regardless of intent.No Requirement to Show Specific Economic Loss: Under the Martin Act, the NYAG can intervene even if investors haven’t suffered actual financial harm, as long as the conduct in question could mislead the public.In essence, the Martin Act is a highly “preventive” law, granting law enforcement near-absolute proactive authority.

2.2 Why Was the Martin Act Created?

In the early 20th century, as the U.S. financial markets expanded rapidly, securities fraud became rampant. Around 1920, states began enacting “Blue Sky Laws” to regulate securities markets. New York State Senator Louis Martin, witnessing widespread investor deception through false securities promotions, introduced the Martin Act in 1921.

The law aimed to protect investors swiftly, given the difficulty of proving fraudulent intent. Initially targeting blatant securities scams, the Martin Act has evolved into New York’s most potent financial regulatory tool.

2.3 What Makes the Martin Act Unique?

The Martin Act’s power is evident in three critical areas:

Concentration of Enforcement Authority: Unlike other laws that allow private lawsuits, the Martin Act centralizes enforcement solely within the NYAG’s office. Investors seeking redress must rely on the Attorney General’s discretion to investigate or prosecute.Broad and Confidential Investigative Powers: The NYAG can initiate investigations without prior evidence of wrongdoing, maintaining strict confidentiality. Subpoenas can be issued to any relevant parties, and leaking information about an investigation can lead to misdemeanor charges.Severe Penalties: Violators face substantial fines, injunctions, and potential criminal charges. Recent examples include Galaxy Digital’s $200 million penalty and the Trump Organization’s $450 million fine, highlighting the Act’s formidable enforcement capabilities.Despite its strength, the Martin Act remained relatively dormant for decades until revived by Eliot Spitzer in 2002 during his tenure as NYAG.

3. The Martin Act in Action

If laws had personalities, the Martin Act would undoubtedly be an aggressive and forceful character. Though enacted over a century ago, it was not until the early 21st century that it fully revealed its power, repeatedly shaking up Wall Street. The most notable cases include the Merrill Lynch scandal, the global settlement with the ten largest investment banks, and the Trump Organization case.

3.1 The Merrill Lynch Case: The Fall of a Wall Street Giant

The first time the Martin Act truly rocked Wall Street was in 2002, with the Merrill Lynch case. The central figure behind the prosecution was Eliot Spitzer, who had just assumed office as the New York Attorney General.

In early 2002, the U.S. stock market was reeling from the burst of the dot-com bubble, leaving investors with massive losses and the public in a state of fear. It was at this time that Spitzer set his sights on Merrill Lynch. He discovered that Henry Blodget, one of the firm’s top analysts, was engaged in severe conflicts of interest: while publicly recommending certain tech stocks to retail investors, he was privately calling them “junk” and “worthless” in internal emails.

For example, Merrill Lynch advised its clients to buy stock in the internet company Infospace, but Blodget described it in private emails as “a piece of crap not to be touched.” Such examples were numerous. These misleading actions caused significant harm to countless retail investors.

Using the Martin Act’s low burden of proof, Spitzer did not need to prove Blodget’s intent to defraud — he simply had to demonstrate that the misleading information had the potential to deceive the public. Merrill Lynch had no way to mount a defense and ultimately agreed to pay a $100 million fine and promised to reform its practices by separating analyst compensation from investment banking revenue. The firm’s reputation was irreparably damaged, and the Martin Act was now firmly feared on Wall Street.

3.2 The Global Settlement with the Top Ten Investment Banks: A Financial Earthquake

But Spitzer’s ambitions did not stop with Merrill Lynch. Next, he set his sights on the core of Wall Street — its ten most powerful investment banks, including Goldman Sachs, Morgan Stanley, and Citigroup.

In 2003, Spitzer’s investigations revealed that conflicts of interest were widespread within these banks’ research divisions. Analysts routinely exaggerated stock prospects to attract investment banking deals, even when they privately admitted that those stocks were worthless.

For instance, Mary Meeker, an analyst at Morgan Stanley, heavily promoted the stock of the tech company Drugstore.com, leading many investors to follow her advice. Yet, in private emails revealed later by Spitzer’s team, she expressed doubts about the company’s outlook, stating that it “was not worth investing in.” The public was outraged upon learning of these internal discrepancies.

Armed with the Martin Act, Spitzer launched an unrelenting investigation. Eventually, all ten investment banks were forced to concede. In 2003, they reached a “global settlement” with regulators, totaling $1.4 billion in penalties.

Specific penalties included $110 million from Goldman Sachs, an additional $200 million from Merrill Lynch, and $125 million from Morgan Stanley. Beyond financial penalties, the banks were compelled to implement strict reforms to separate their research and investment banking operations, establishing an institutional “firewall” to prevent future conflicts of interest.

This case, widely recognized as the largest and most impactful financial settlement in Wall Street history, marked the Martin Act’s moment of peak influence. From then on, conflicts of interest between analysts and bankers became an untouchable red line — one that continues to haunt the financial industry today.

3.3 The Trump Organization Case: Not Even a Former President Can Evade the Martin Act

While the Merrill Lynch and top ten banks cases demonstrated the Martin Act’s power over Wall Street, the Trump Organization case showed that it could reach even the most politically sensitive figures.

In February 2024, New York Attorney General Letitia James invoked the Martin Act to sue former President Donald Trump’s business empire. The Trump Organization was accused of consistently and grossly inflating asset values to secure favorable loan terms and insurance policies.

Investigations revealed that the company had wildly overstated property values. For instance, the Trump Tower in Manhattan was reportedly valued at around $500 million, yet the Trump Organization told banks it was worth over $2 billion. Dozens of similar incidents were uncovered, severely misleading financial institutions.

Because the Martin Act does not require proof of intent, but merely the potential to mislead, the court swiftly ruled that the Trump Organization had committed fraud. The penalty was $450 million, and Trump along with his family businesses was restricted from conducting commercial activities in New York State.

Although Trump strongly denied the charges, he could do little against the Martin Act’s clear provisions and low evidentiary threshold. The judgment dealt a heavy blow to his business empire and sent a chilling message across political and financial circles about the Martin Act’s relentless reach.

3.4 Summary: The Martin Act’s Side Effects and Controversies

Through the Merrill Lynch case, the global investment bank settlement, and the Trump Organization suit, it becomes clear that the Martin Act has become the Attorney General’s ultimate tool for policing New York’s financial markets. Any improper behavior related to securities or financial products within the state is unlikely to escape its net.

However, with such sweeping powers come serious concerns. Many in the financial industry believe that the Act’s low enforcement threshold may lead to regulatory overreach, stifling innovation and subjecting companies to massive penalties for minor infractions.

That said, I believe that — when it comes to the cryptocurrency market — the Martin Act may well be a godsend.

4. Why the Martin Act Is a Gifted Blade for Crypto

Some may find it strange that such a harsh legal weapon, one that strikes so heavily at financial firms, could be seen as anything but a threat to innovation. Many in the crypto community view the Martin Act as a “warlord’s blade,” one that swings wildly and risks harming the innocent.

But I want to offer a different perspective: in today’s chaotic crypto landscape, the Martin Act may be nothing short of a divine opportunity to bring order and legitimacy to the industry.

Why do I say this?

In one phrase: extraordinary times call for extraordinary measures.

4.1 Just How Chaotic Is the Crypto Market?

Even the most optimistic believers must admit that the crypto market is wildly chaotic. In just a few short years, the space has become a hotspot for global financial fraud. A staggering variety of scams have emerged, many of which leave investors defenseless.

Let’s look at some data:

According to the FTC’s March 2025 report (New FTC Data Show a Big Jump in Reported Losses to Fraud to $12.5 Billion in 2024), crypto-related scams resulted in $1.4 billion in losses in 2024, while investment scams accounted for $5.7 billion. The total fraud losses hit $12.5 billion, showing a sharp upward trend.

Globally, the numbers are even more alarming. Chainalysis’ 2024 Crypto Crime Report states that global crypto fraud reached $19 billion, a 55% year-over-year increase.

The types of scams are constantly evolving. Here are a few major ones:

(1) The Classic “Rug Pull”

In early 2022, the Squid Game Token exploited a viral IP to pump its price tens of thousands of times within days. At the peak, the project’s creators suddenly withdrew all liquidity, vanishing with over $3.3 million in assets. Investors watched helplessly as their holdings went to zero — all in mere minutes.

(2) Pump-and-Dump Schemes

Luna, the token involved in Galaxy Digital’s controversy, is a prime example. Mike Novogratz promoted Luna heavily on Twitter, branding it as the “next-generation stablecoin king.” Meanwhile, he was quietly selling his holdings. Retail investors were left to hold the bag after the price crashed. According to CoinGecko’s 2023 data, over 60% of new crypto tokens crashed within 90 days of launch — many due to obvious market manipulation.

(3) Ponzi Schemes Disguised as Innovation

The most infamous examples are Terra/Luna and FTX.

Terra’s founder Do Kwon promised 20% annual returns via the Anchor Protocol, attracting over $60 billion in deposits in a single year. But the system operated like a Ponzi scheme: new investors’ funds were used to pay old ones. When inflows stopped, the entire ecosystem collapsed — millions of investors lost everything.FTX was even more absurd. Founder Sam Bankman-Fried appeared in media as a philanthropic genius, yet behind the scenes, he misused client funds to support risky trades by Alameda Research. When the truth came out, the $32 billion exchange evaporated overnight.

Besides these headline cases, retail investors constantly face phishing attacks, insider trading, and hacks. According to PeckShield’s Q1 2025 report (Crypto hacks top $1.6B in Q1 2025 — PeckShield), hacking losses totaled $1.63 billion, a 131% increase from Q1 2024, involving over 60 major incidents.

These hacks might be beyond the Martin Act’s reach, but they are part of the same crisis that deters millions from trying decentralized finance. Make no mistake — these are crimes, often coordinated and sometimes even backed by state actors. We will cover that in detail another time.

4.2 Why Is the Crypto Market So Chaotic?

The mess in crypto did not arise from nowhere. It stems from a tangle of regulatory gaps, technical complexity, moral hazard, and a culture that resists oversight.

First, a Regulatory Vacuum

Over the past decade, crypto has grown at a pace regulators could not keep up with. Agencies like the SEC and CFTC have long debated whether Bitcoin, Ethereum, and other altcoins are commodities or securities, leaving the market in a legal gray zone.

When FTX collapsed in late 2022, Patrick McHenry, chair of the U.S. House Financial Services Committee, lamented, Our slow response enabled a scam like FTX to grow unchecked.

Second, Technical Complexity and Asymmetric Information

Blockchain is complex. Most investors cannot assess project quality, while insiders and exchanges control almost all critical data.

In Terra’s case, Anchor’s 20% APY seemed irresistible, but the mechanism behind it was opaque. Retail investors followed influencer endorsements blindly — and were the last to exit.

Just before FTX’s collapse, Sam Bankman-Fried publicly claimed the exchange was solvent. Investors had no way to verify reserves. This kind of black box environment makes scams easy to execute.

Third, Moral Hazard Driven by Profit

Crypto liquidity is high. Anyone can launch a token, get listed, and cash out quickly.

As of April 2025, CoinMarketCap lists over 13 million tokens, but fewer than 100 have real utility. The rest are mostly “junk coins” or “air coins.” With huge wealth at stake, project teams, exchanges, and capital often collude to manipulate markets.

Fourth, Media Amplification

Mainstream and social media often hype projects irresponsibly for views and profits.

Twitter, Reddit, and Telegram are full of paid shills and influencers pumping coins. According to CoinDesk, false promotions on social media caused investors over $1 billion in direct losses in 2023 alone.

Most retail users cannot discern genuine analysis from manipulation.

Fifth, Misuse of Decentralization Ideals

Crypto’s anti-authoritarian spirit has been weaponized. Many DeFi projects refuse to disclose team identities or undergo audits, hiding behind decentralization.

When users lose funds to hacks, these projects often refuse compensation, citing “decentralization means user risk.” This ideological abuse fuels disorder.

Lastly, Lack of Industry Self-Discipline

Traditional finance developed strong compliance cultures over decades. Not so in crypto.

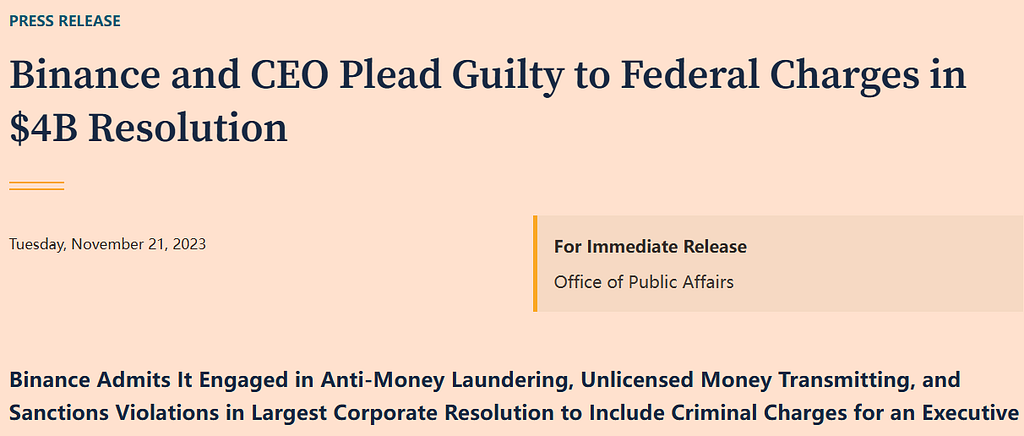

Even top exchanges like Binance and Coinbase face regular allegations of insider trading and misconduct. In November 2023, Binance and CEO Changpeng Zhao admitted to money laundering and sanctions violations, paying over $4 billion in fines (DOJ report).

Taken together, the chaos of crypto stems from a complex interplay of slow regulation, opaque data, profit-driven actors, and ideological cover. These factors turn the market into a “Wild West” — a perfect hunting ground for scammers.

And it is precisely in this context that the Martin Act’s true value becomes clear.

4.3 Why the Martin Act Is a Sword, Not a Shackle

There’s an old saying: “History does not repeat itself, but it often rhymes.” The chaos we see in today’s crypto markets mirrors almost exactly the disorder of the early 20th-century U.S. stock market — proving this maxim once again.

Let us rewind the clock to the early 1900s. At that time, the American stock market was experiencing what was later dubbed the “Wild West” era. Much like today’s crypto markets, Wall Street back then was flush with gold, brimming with opportunity — and riddled with scams. The environment was a free-for-all.

There was no SEC, no standardized securities laws, and no legal constraints. Wall Street became a haven for fraudsters. Market manipulation, insider trading, and fake promotions were rampant.

One of the most infamous manipulators was “The Boy Plunger,” Jesse Livermore. In the early 1920s, he leveraged his massive capital to spread false news, collude with brokers to drive up stock prices, and then dumped his holdings at the top. During the 1929 crash, Livermore made over $100 million (worth several billion today), while millions of ordinary investors lost their life savings overnight.

The securities market at that time resembled today’s crypto market: no mandatory disclosure, no auditing, and no responsibility to investors. Companies could issue stock freely, with no requirement to publish financial statements. Brokers could manipulate prices at will. Retail investors were little more than sheep to be slaughtered.

A famous example from that era is Charles Ponzi’s scheme. He promised investors a 50% monthly return through a postal coupon arbitrage operation. In reality, it was a classic Ponzi setup: using new investors’ money to pay off earlier ones. Within a year, he amassed over $20 million (hundreds of millions in today’s dollars). When the scheme collapsed, the fallout was devastating.

It was in this lawless environment that states across the U.S. began to introduce some of the earliest securities laws — known as Blue Sky Laws. The Martin Act, enacted in 1921, was New York’s response. It was born during one of the most fraudulent, unregulated periods in the state’s financial history, designed to protect everyday investors from predatory scams.

The Martin Act quickly made an impact. It imposed strict standards on stock issuers and brokers, punished false advertising and deceptive conduct harshly, and signaled a new era of accountability.

During the 1920s and 1930s, it was used to crack down on fraudulent oil companies, real estate scams, and other major schemes. These swift and severe actions helped restore order to New York’s markets.

Then, in 1934, the U.S. Securities and Exchange Commission (SEC) was established, and the Securities Exchange Act was passed, drawing on the experiences of the Martin Act and other state-level laws to enforce regulation at the federal level.

That strong regulatory foundation is what helped shape the U.S. stock market into what it is today: the most liquid, transparent, and trusted capital market in the world.

Now, look at today’s crypto space. We are once again in a time of explosive, unchecked growth. An average of 56,000 new tokens are created every day. The total number of crypto assets exceeds 13.24 million. While innovation flourishes, scams run just as wild.

In this landscape, we are once again in desperate need of a strong regulatory sword to bring an end to the chaos and allow the space to mature.

Yes, the Martin Act is strict — even unforgiving. Its low burden of proof and heavy penalties make many uncomfortable. But if history has taught us anything, it is that true market fairness must be built on the back of legal deterrence. Those who recklessly violate rules will only respond to real consequences.

Crypto’s current disorder echoes the early days of the stock market. By learning from history, we should recognize the Martin Act as a century-old sword — flawed, perhaps, but powerful and necessary. It can slash through fraud and deceit to make room for real, lasting innovation.

Conclusion

History does not simply repeat — it rhymes in remarkable ways.

One hundred years ago, the Martin Act was born in the chaos of Wall Street; a century later, it is being summoned again to rescue the crypto market now drowning in a tide of scams and disorder.

Some claim, “Regulation is the enemy of innovation.” But history tells us otherwise: without regulation, innovation becomes a playground for fraud. Wall Street’s enduring prosperity is not the result of unbridled freedom, but of the sharp legal sword standing guard behind it.

In the world of finance, there can be no safety without reverence, no future without regulation. The Martin Act may be a blunt instrument — it is sharp, and it cuts deep — but what it severs is not the path of innovation, but the vines of deception and greed. Law does not hinder true innovation; it only clears the way by cutting down those who masquerade as innovators.

A truly valuable free market does not fear the sword of justice.

The Martin Act may not be perfect, and it may not be the answer to every problem, but in an industry spinning out of control, it remains a blade that protects the ordinary investor — flawed, yes, but essential.

The Martin Act Targeting the Crypto Industry? was originally published in The Capital on Medium, where people are continuing the conversation by highlighting and responding to this story.

Bengali (Bangladesh) ·

Bengali (Bangladesh) ·  English (United States) ·

English (United States) ·