Kyle Prevost, creator of 4 Steps to a Worry-Free Retirement, Canada’s DIY retirement planning course, shares financial headlines and offers context for Canadian investors.

Shopify struggles

Canada’s second-largest company (or third, depending on the day) had a relatively strong earnings day on Tuesday, but the company’s share price took a beating based mostly on decreased earnings expectations going forward.

Shopify earnings highlights

Shopify is listed on both the Toronto and New York Stock exchanges, and it announces earnings in U.S. dollars.

Shopify (SHOP/TSX): Earnings per share of $0.34 (versus $0.31 predicted), and revenues of $2.14 (versus $2.08 predicted).Shares of Canada’s tech darling were down over 13% on Tuesday, but even with the massive pullback, the share price is still up 14% year to date (YTD).

Shopify’s CFO Jeff Hoffmeister reported the good news that more products were sold on the Shopify platform than ever before. The fourth quarter included the all-important holiday shopping activity, and Hoffmeister announced that Shopify has moved $75.1 billion-worth of merchandise. That was a 23% increase on last year’s numbers. Net earnings came in at $657 million, compared to a loss of $623 million during the fourth quarter in 2022.

President Harley Finkelstein said Shopify handled the orders for 61 million customers worldwide on the Black Friday weekend.

“Our platform handled a staggering 967,000 requests per second, which is the same as 58 million requests per minute, nearly 80% higher than our peak traffic just two years ago.”

—Harley FinkelsteinSo, where’s the struggle? Growth is not the same as profitability. With Shopify stating its free cash flow is going to be substantially lower than previously indicated, investors were quick to pounce on the bad news.

Finkelstein tried his best to put a positive spin on future growth opportunities.

“There are opportunities for us to go beyond Europe. Of course, we’ve talked about Latin America and the Asia-Pacific in the past, but we definitely see a lot of opportunity there[…] I mean, we’ve captured less than 1% of market share in global retail sales, even as our product and geographies have expanded.”

There’s no question Shopify’s been an incredibly innovative company, and it is all the more noteworthy for keeping its home base in Canada, despite many tech companies moving shop. It’s very likely the company will be consistently profitable, but trying to forecast the “when” and the “how much” of that long-term profitability is a very difficult endeavour. In this age of higher-for-longer interest rates, investors appear to be demanding durable profits sooner rather than later, and consequently, shareholders will have to buckle up for a bit of a volatile rollercoaster.

Can Shopify keep up the growth momentum while controlling costs? Investors are betting on it. But Tuesday’s dip would indicate that it’s not at all certain about those bets.

Canadian pipelines and utilities—boring and very profitable

Two of Canada’s largest midstream companies reported earnings this week.

Pipeline and utilities highlights

Here are two Canadian earnings reports that made headlines this week.

Enbridge (ENB/TSX): Earnings per share of $0.64 (versus $0.66 predicted), and revenues of $11.30 billion (versus $13.35 predicted). Keyera (KEY/TSX): Earnings per share of $0.21 (versus $0.53 predicted), and revenues of $1.78 billion (versus $1.64 predicted).The huge discrepancy between pipeline company Keyera’s earnings-per-share and the predicted figure apparently stemmed from one-time costs not included in analysts’ predictions. In any case, the market didn’t think there was much cause for concern as the share price was almost flat after earnings were announced on Wednesday. Certainly, it’s an improvement on last year’s loss of $0.37 per share.

Keyera’s earnings statement highlighted its commitment to strengthening its balance sheet, with net debt to adjusted EBITDA at 2.2x, which is substantially below the target of 2.5x to 3.0x.

Clearly the current interest rates are weighing on the pipeline company’s ability to leverage more capital spending. With a dividend payout ratio of 53% of free cash flow, Keyera’s ability to pay its dividend looks quite secure for the time being.

Enbridge, on the other hand, decided to leverage substantially more money than Keyera. Its debt-to-EBITDA ratio is 4.1x (earnings before interest, taxes, depreciation and amortization).

President Greg Ebel said, “Our stable, low-risk, diversified business remains well positioned to grow earnings and dividends for shareholders for years to come.”

The Canadian market doesn’t appear to really trust Enbridge, though, as the share price was down on the day despite the announcement of a 3.1% increase to the company’s dividend. While it is the utilities company’s 29th consecutive year with a dividend increase, shareholders no doubt miss the days of 10% dividend increases.

In an effort to control costs, last month, Enbridge announced it would be cutting 650 positions because of geopolitical instability, persistent inflation and rising interest rates. Interest rates can’t come down soon enough for capital-intensive industries, like pipelines that have to borrow large amounts of money as a necessary part of its business model. Its 8%+ dividend doesn’t appear to be in any immediate danger, but shareholders are clearly getting a bit suspicious about the long-term future of the company. Share prices are down over 5% YTD.

Canadian utilities highlights

Two large Canadian utilities produced steady results this past week, as one might expect from the heavily-regulated sector.

Fortis (FTS/TSX): Earnings per share of $0.53 (versus $0.53 predicted), and revenues of $2.88 billion (versus $3.02 billion predicted). Hydro One (H/TSX): Earnings per share of $0.30 (versus $0.30 predicted), and revenues of $1.98 billion (versus $1.5 predicted).For more information, you can check out my articles on Canadian utility stocks and Canadian pipeline stocks at MillionDollarJourney.ca.

Earn between 2.5% and 4% interest on your savings. Plus, use the pre-paid card for everyday purchases and free ATM withdrawls.

$0 commission on all transactions. No minimum deposit needed.

Interest rate: 5.40%

MoneySense is an award-winning magazine, helping Canadians navigate money matters since 1999. Our editorial team of trained journalists works closely with leading personal finance experts in Canada. To help you find the best financial products, we compare the offerings from over 12 major institutions, including banks, credit unions and card issuers. Learn more about our advertising and trusted partners.

Cameco’s painting a bigger picture

Last week Cameco had a rough earnings day, and subsequently its stock is down 11.5% over the last five trading days.

Cameco’s earning highlights

Here’s what the nuclear company reported this week.

Cameco (CCO/TSX): Earnings per share of $0.21 (versus $0.25 predicted), and revenues of $844 million (versus $814.69 million predicted).This is a stark contrast to its third-quarter earnings call in 2023, which saw it massively outperform expected earnings.

Perhaps, more importantly, we should place this relatively small earnings miss in the right context. Cameco’s returns over the last 12 months, and five years actually, have been excellent.

Source: Google Finance

Source: Google Finance

Source: Google Finance

Source: Google Finance

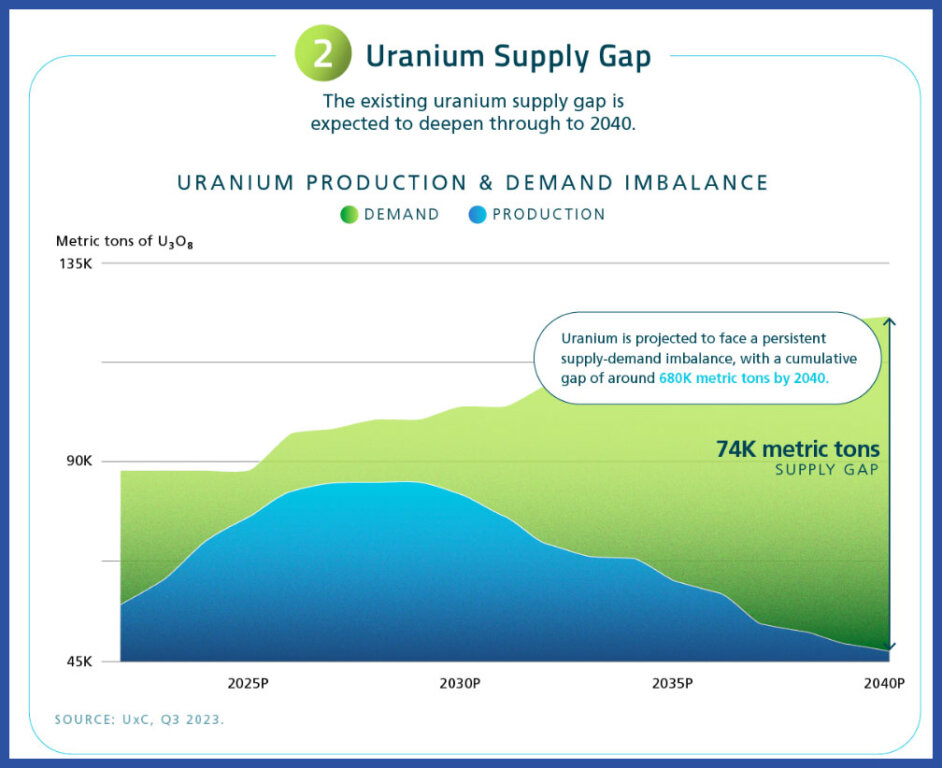

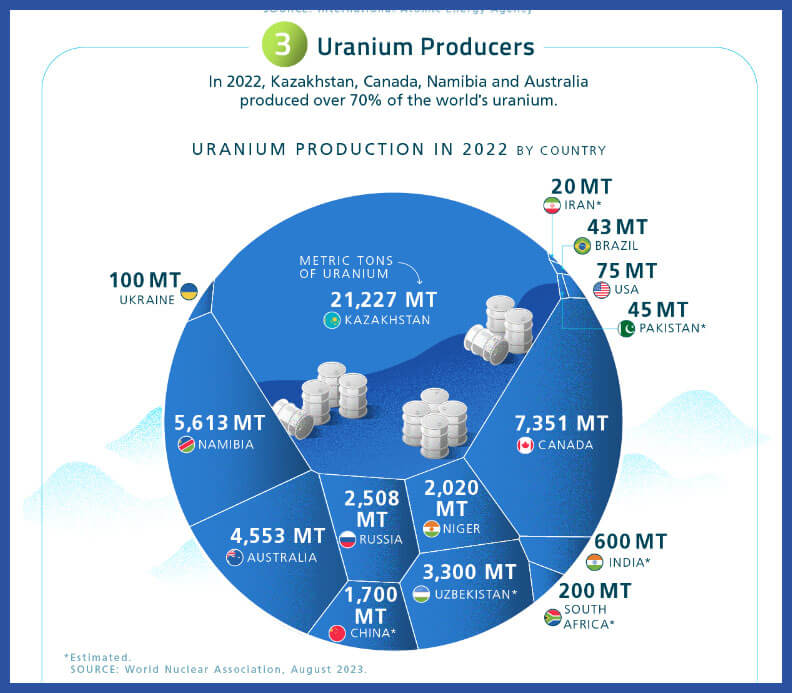

The bulk of Cameco’s story likely has yet to be told. There’s no question that a company solely focused on taking uranium out of the ground is looking at a bright future. As always, the real quandary is: Has the market already priced in this growth?

“In today’s environment, the uranium market is certainly having more than just a moment. Instead, we’re seeing full-cycle growth in the near, mid- and long-term with broad interest in nuclear energy like never before. And it’s being driven by global scale factors that are widely expected to persist for years to come […] There’s a growing consensus that there is no net zero without nuclear.”

Tim Gitzel, Cameco CEO, following at the earnings press conferenceUranium spot prices doubled in 2023 and it looks like that trend is set to continue for a while.

Source: Visual Capitalist

Source: Visual Capitalist Source: Visual Capitalist

Source: Visual Capitalist

Given that Cameco produces about 17% of the world’s uranium, and that much of Kazakhstan’s ability to transport uranium goes through sanction-impeded territory in Russia, it could be argued that there isn’t a better way to bet on uranium and nuclear energy than through this Saskatchewan-based company.

Notably, Cameco is involved in a joint venture in Kazakhstan, and it recently acquired a nuclear services company in the United Kingdom. So, there is growing geographical diversity to the company’s assets as well.

As Gitzel said at the press conference, the general feeling around nuclear energy appears to be less and less influenced by the tragic events at Fukushima in 2011. It’s more reflective of the reality around the shift to non-carbon-based energy. Wind and sun may not be the long-term answer to 100% of our energy needs, and Cameco looks to be ready to capitalize on that.

The increased costs and operational issues that hurt Barrick

With gold sticking close to USD$2,000 per ounce, it’s no surprise that the second-largest gold company in the world continues to be quite profitable. Like Shopify, Barrick announces its earnings in U.S. dollars, as the company is listed on the NYSE andthe TSX.

Barrick’s board of directors shared the following highlights in regards to its fourth quarter:

Barrick has one of the mining industry’s strongest balance sheets with essentially no net debt. Free cash flow was 50% higher in 2023 than in 2022. The $0.10 dividend (currently yielding just under 3%) will be maintained for 2024. A $1 billion share repurchase program will take place in 2024 after zero shares being bought back in 2023.The market reacted mildly positively to the announcement, with the share price up about 1.5% in after-hours trading on Wednesday.

Mining earnings highlights

Barrick Gold’s latest earnings report.

Barrick Gold (ABX/TSX): Earnings per share of $0.27 (versus $0.21 predicted), and revenue of $3.06 billion (versus $3.14 billion predicted).This earnings news only served to shine what had been a pretty dull start to the year for Barrick. In mid-January, the company had equipment issues at its Dominican Republic mine, and lowered output at the Nevada Gold Fields project meant that the total gold mined in 2023 was going to come in 2% to 3% under initial estimates. Additionally, total cost per ounce was now going to be 8% to 10%, which was slightly higher than it had forecasted. Consequently, Barrick’s share price is down about 20% so far in 2024.

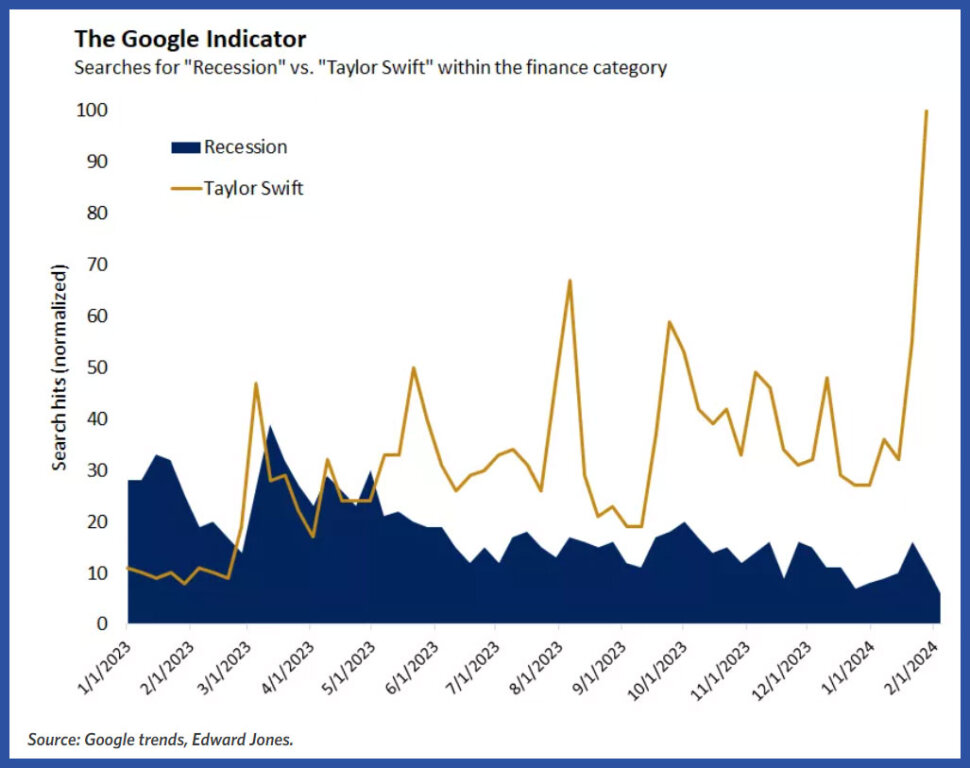

Our moment of Zen

In honour of Jon Stewart back on The Daily Show this week, we thought we’d sign off with a “moment of Zen” that celebrates the big picture for investors.

It’s good news for economic sentiment when searches for “Taylor Swift” outnumber those for the term “recession.” Clearly people now feel that we have other things to worry about.

Source: Edward Jones

Source: Edward Jones

Read more about investing:

How might inflation impact your retirement plans? What is a cashable GIC? Will GIC rates keep going up in 2024?The post Making sense of the markets this week: February 18, 2024 appeared first on MoneySense.

Bengali (Bangladesh) ·

Bengali (Bangladesh) ·  English (United States) ·

English (United States) ·