2 hours ago

3

2 hours ago

3

As prices go up on everything we pay for, it’s critical that we don’t overpay on any of the big bills we get. While you can’t do much about your rent or your mortgage, one big annual bill that deserves attention is insurance.

I’ve made it my mission to pay as little as possible for car insurance. As a relatively safe driver, I’ve been fortunate to qualify for various discounts but there’s always more you can do.

Here are the things I’ve done to reduce it:

Table of ContentsShop AroundImprove Your Credit ScoreUpdate Your Annual MileageIncrease Your DeductibleBundle Bundle BundleAdjust Your Coverage With AgeAsk Your AgentShop Around

Obviously, first step is to comparison shop. This is the biggest bang for your buck, as insurance companies compete like crazy for your business and you should take advantage of it.

Find out if you can get insurance for cheaper elsewhere. If you haven’t done a check in a year or two, takes a few minutes to confirm you’re can’t just switch and save hundreds.

You can sometimes bring this offer to your existing insurer and they will do what they can to match or beat it.

👉 Check if you’re overpaying on car insurance

Improve Your Credit Score

In many states, your credit score is used to determine your insurance rates because it’s predictive of future claims. You can reduce your rates by taking these steps to improve your credit score.

Not every state allows this though. California, Hawaii, Massachusetts and Michigan do not allow insurers to use that information to set rates. Maryland, Oregon, Utah, Washington, Nevada, and North Carolina set restrictions on how much they can use it… but every other state allows it.

They don’t use your FICO credit score, they use a proprietary credit-based insurance score but it follows many of the same factors as your actual credit score… so improving it will help.

Update Your Annual Mileage

I work from home and so my annual mileage is typically much lower than the average American who commutes 27 minutes a day. (source) When I told my insurance agent, they were able to lower my premiums because fewer miles on the road means less risk.

In my case, they didn’t need to know the actual mileage. They just recorded that I worked from home and I didn’t commute every day. As a result, I don’t have to confirm my mileage each year.

Your insurance company may treat this differently. Some require you to estimate your actual mileage, send in your odometer readings each year, but it’s still worth checking if your mileage is considered “low” by the company.

Increase Your Deductible

Every insurance policy has a deductible, which is what you will pay on each claim before the company does. The higher the deductible, the less you’ll pay in premiums because you’re taking on more of the risk.

A policy with a $1,000 deductible is much cheaper than one with a $500 deductible. If you can afford to take on the risk, tell your insurance company you’d like to raise your deductible.

It’s important that if you do this, you increase your emergency fund accordingly.

(if you are a renter, don’t forget renter’s insurance!)

Bundle Bundle Bundle

This sounds silly but I had bundled our car and homeowners insurance but I originally didn’t bundle our umbrella insurance. Sometimes you get things at different times and you don’t really think about it… but I did and it saved us a bunch.

Insurance companies love this because it makes switching insurers just a little bit harder. It also means they earn more from you so they’re willing to take a little discount on premiums to earn more of your business. They do the same amount of administrative work but they collect more money.

That said, don’t assume bundling is cheaper than going a la carte. Sometimes you can save money by separating too, so price it out to confirm.

Adjust Your Coverage With Age

When I owned an older car, I adjusted the coverage based on how much risk I was willing to take and how much the car was worth. You can play with deductibles here too but in my case, I decided to remove comprehensive insurance.

Comprehensive insurance is the part of your auto policy that protects your vehicle from non-crash damage. If your car hits another car, collision insurance protects your car. If you hit a pole, collision insurance covers your car. If you open the door into a pole, that’s comprehensive.

(quirky enough, if someone breaks into your car and steals something… that’s actually renters or homeowner’s insurance)

Basically if you damage your car and it doesn’t involve another car, it’s comprehensive. If your car is only worth a few thousand dollars, paying several hundred dollars a year for comprehensive and collision coverage may no longer make financial sense.

Ask Your Agent

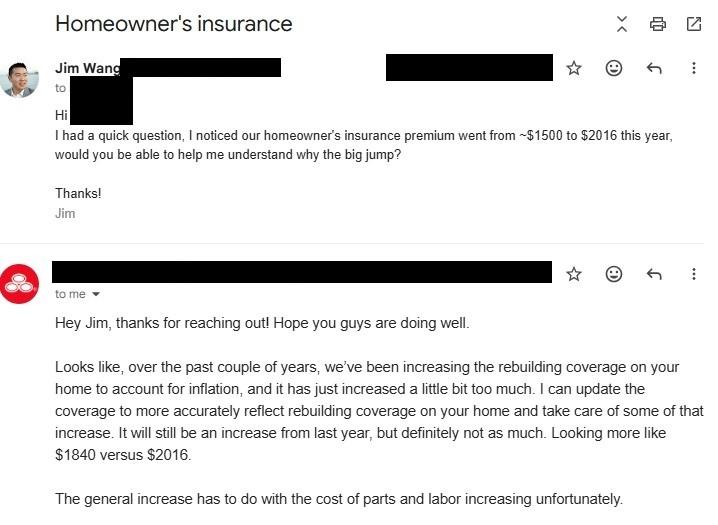

Finally, sometimes it pays to just ask your agent if there are ways for you to reduce your bill. When my homeowners policy was up for renewal, there was a sizable jump in the annual premium. I asked my agent why and we were able to come up with ways to reduce it that didn’t impact my coverage:

I’ve had several conversations with her over the years and while not all of them involved in a reduction, we did find a few ways to reduce the bill. Every time I’ve hung up, I’ve felt better informed and happy about where our rates were.

Here are a few things to ask about:

affinity discounts paperless billing autopay defensive driving course discounts good student discounts low-mileage programs multi-car discountsYou may be able to find a way to lower your bill even more!

The post 7 Real Ways I’ve Lowered My Car Insurance Bill appeared first on Best Wallet Hacks.

Bengali (Bangladesh) ·

Bengali (Bangladesh) ·  English (United States) ·

English (United States) ·